Foreign workers sending money back home electronically — digital remittance — is a powerful driver of economic growth. Improving the capabilities and reach of this money transfer channel has a material impact on people’s lives and is a significant business opportunity.

As the pandemic has slowed down cross-border money flows, many remittance companies have had to learn how they can operate in a digital-first environment. They need to control costs to offer their customers lower fees, while still maintaining profitability. They also must ensure they meet compliance obligations and position themselves for substantial long-term growth.

Besides a general economic slowdown, the pandemic has had significant impacts on worker migration. The World Bank projects that remittance flows to low- and middle-income countries will fall 7.5% in 2021, after a 7% drop in 2020. (It’s important to note that the World Bank initially projected a 20% drop for the year in April 2020, so although the decline wasn’t as bad as initially forecast, it’s still significant.)

The resulting economic pain affects both personal lives and national economies. Before the pandemic, over 270 million people worked outside of their home country, sending back money that accounted for more than 5% of the GDP in 60 developing countries. These funds are often critical to the economic survival of the recipients.

Shifting to digital remittances

Traditionally, remittances involved multiple parties, lots of paperwork, slow transfers and high fees. Often, both the sender and receiver have to go to a physical location to send or collect their money, which has become problematic due to pandemic-related restrictions.

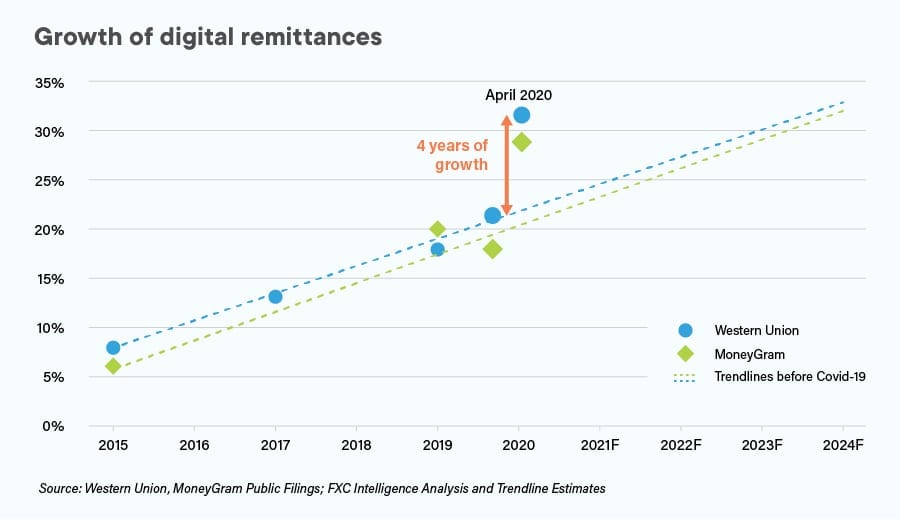

Fortunately, digital remittances were already a growing trend, so many remittance companies had some preparation for the rapid shift to online and mobile channels. An article in Forbes noted that “money transfer companies squeezed four years of digital growth into just two months.” WorldRemit saw 150% year-on-year growth in the first months of the pandemic. MoneyGram saw a 17% increase in digital revenue in Q1 2020, while Western Union saw a 13% increase.

From Forbes: Western Union and MoneyGram share of digital transactions FXC INTELLIGENCE

From Forbes: Western Union and MoneyGram share of digital transactions FXC INTELLIGENCE

Digital remittances solve many of the problems of sending money cross-border to a person in a low- or middle-income country:

- Cuts travel to a specific location to send or receive money. With the increased use of mobile money apps, people can save significant travel time

- Decreases lengthy delays in receiving funds. Traditional remittance transfers often rely on numerous intermediaries. Each has an incentive to delay the transfer, as they can have the funds on their books for some time. Depending on the specific payment channel, an international transfer can take 3-5 business days, but any complication can substantially increase delays

- Lowers the cost of high fees. With so many parties involved, costs can rise to take a significant portion of the remittance. While the UN Sustainable Development Goal calls for a transaction fee of 3%, average transaction fees are 6.5% (and can reach 10% or more in some remittance corridors)

The bumpy road to adopting digital remittance

While digital remittance might seem like a panacea to all money transfer problems, there are fundamental issues around adopting new technology. Many people in developing countries don’t trust technology when it comes to something as essential as money.

People are used to buying food and paying bills with currency and coins. Asking them to now trust a phone is a major psychological hurdle, no matter the profound benefits.

Of course, there are other factors. While just over 40% of populations in low- and middle-income countries have mobile internet, that still leaves a substantial number of people with no access. There needs to be widely available payment services that are known and trusted by the local population. People must understand how to use the systems and protect their money and cost structures need to make sense for the market.

Perhaps a silver lining of the pandemic — if something so devastating can have a benefit — is that people have had to rely on no-contact digital processes. If the only way to get funds is using digital remittance, then people are now more willing to try it. It’s uncertain what will happen when traditional channels become available again, but perhaps resistance will lessen as people become more familiar with the technology and trust it.

The digital tip of the iceberg

It’s vital to understand that this growing acceptance of digital remittances is an indicator of the new digital economic reality.

According to the World Bank, 65% of adults in the developing world lack access to essential financial services. Their lives are more burdensome as it’s more challenging to save money, build up credit, pay bills or otherwise participate in the financial system.

But there are also indicators of digital money adoption in developing economies. In Kenya, 72% of the population already has a mobile money account. In a 2019 infographic, GSMA states that over 1 billion have mobile money accounts globally; it also pointed out that the average cost of sending $200 was only 1.7%. A pre-pandemic estimate had the amount for digital remittance transactions overtaking traditional methods by 2023.

Receiving a digital remittance into an account is a potential game-changer. As the person starts to use the account, they can build the necessary comfort level and trust in transacting digitally. They can start using the account to receive money, save, pay bills, and use it as a full-functioning financial account.

In that light, all the investment in money, time and energy to build effective digital remittance channels now are a down payment in delivering a full range of financial services to billions of new consumers. As an article in Forbes puts it, that is a $100 trillion opportunity:

Serving the unbanked will generate some of tomorrow’s largest fortunes. It is both capitalism’s moral imperative and the route to one of the most significant untapped markets.

Digital remittance systems that can work in different markets, that provide regulatory compliance while also delivering a simple and straightforward user experience, will enable companies to onboard more customers and position themselves for the next phase of growth. Acquiring customers now, in this introductory phase of digital financial services, is an opportunity to establish financial relationships and build trust that is unprecedented and may never occur again.

Solutions

Payment Service Providers

Ensure KYC Compliance With Complete Identity Verification

Resources Library

Payments

Industry Sheets

Digital Identity Verification Can Pave the Way for Payments Industry Compliance and Growth

Featured Blog Posts

Business Verification (KYB)

Enhanced Due Diligence Procedures for High-Risk CustomersIdentity Verification

Proof of Address — Quickly and Accurately Verify AddressesBusiness Verification (KYB)

How to Verify Legitimate Businesses and Merchants