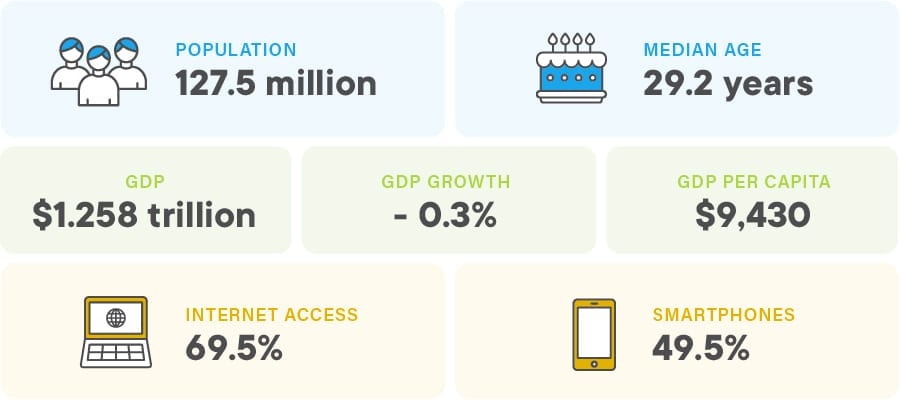

Mexico has a population of 127 million people (2019), the second-largest economy in Latin America and ranks in the top 15 of the world’s largest economies. As a member of the United States-Mexico-Canada (USMCA) trade agreement, it has access to the massive U.S. market next door. With a hyper-connected population and a quickly growing middle class, Mexico is an important market for businesses looking for significant growth opportunities. As it is considered one of the world’s most advanced developing countries, some predict it will become the 7th largest economy of the world by 2050.

Mexico quick stats (2019)

Developing fintech

In terms of fintech, Mexico already has many elements of a sophisticated ecosystem in place. According to Catalyst Fund, there are over 400 fintech companies in Mexico, and with two-thirds raising venture capital. Thirty percent of Mexicans are classified as digital natives, people who are comfortable with online and mobile services and prime candidates for fintech products and services.

A set of laws to guide fintech — The Law to Regulate Financial Technology Companies (the Fintech Law) — improves clarity for both Mexican and international companies looking to expand there. The Fintech Law has a category for electronic money institutions (EMI) which defines rules for sectors such as electronic payments. Included are specific rules for KYC, which define various risk levels according to monthly transaction levels.

In 2019, Mexico updated its AML law, the Federal Law for the Prevention and Identification of Transactions with Funds from Illicit Sources. Regulated parties, according to the FATF, “are generally prohibited from opening or maintaining anonymous accounts.” An exception is made to promote financial inclusion for deposits of pesos into individual accounts that don’t exceed a threshold. For financial transfers above USD $1,0000 basic customer information is required, while amounts over $5,000 require full customer due diligence procedures. Further regulations and AML provisions vary based on the industry and regulator.

Mexican identity verification has grown in the past few years. While there has not been a legal requirement for independent verification, copies of identification are generally provided upon account openings. Furthermore, the verification of Mexican identities is important for many U.S. businesses.

For low threshold customers, simple due diligence procedures are sufficient. As 50% of Mexican adults remain unbanked, making it as easy as possible to onboard these customers can improve the inclusion rate. With only 4.1% of Mexicans using mobile money accounts, companies that can find the right product-market fit have a big market opportunity.

Note, there are reasons why the banking participation rates are so low. As an article in Bloomberg puts it “in Mexico, cash is still king. And, if anything, its use keeps growing, the result of a deep-rooted informal economy and an ingrained distrust of major institutions.”

In 2019, Mexico launched the Cobro Digital (CoDi) payment platform, which uses QR-codes and near-field communication (NFC) technology to perform no-fee transactions through mobile phones. While three million people have downloaded the app, only 167,424 users have made payments through CoDi (as of July 1, 2020). COVID-19 obviously had an effect on the roll-out, but the lack of use also points to other issues including awareness of the platform, competing solutions and mistrust in technology and government.

Effective fintech solutions could also help on the business side of things in Mexico. According to an article in PYMNTS “it can take four to six months to open a business account — and as much as a year to get access to a debit card.” Speeding up and simplifying business processes with various digital transformative techniques will be especially valuable once the pandemic is over and the country can focus on rebuilding. Unfortunately, Mexico is having severe issues with the pandemic.

Identity systems in Mexico

Digital ID — Various, including Clave Única de Registro de Población card

Mexico has a number of identity systems. The Clave Única de Registro de Población (CURP) or Unique Population Registry Code is a registration number assigned to Mexican citizens and residents. People can obtain a CURP card that includes name, CURP code, date of registration and a barcode.

Areas for development

The CURP is intended to be a unique code, but in practice people can obtain multiple codes. As a result, the voter identification database, which uses biometric deduplication, has become a de facto national identity source. For example, voter identification is used for Know Your Customer verification for account opening.

The ID4D World Bank diagnostic on Mexico provides a detailed analysis of the country’s identity ecosystem and steps for improvement.

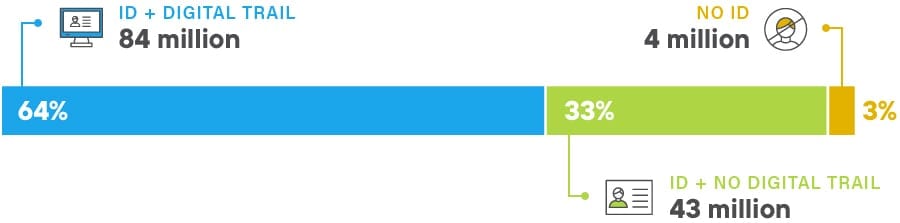

Mexico has made strong progress in issuing ID to all of its citizens. In 2014, the country amended its constitution to include a right to identity and registration immediately after birth. The following year, Mexico launched a modern birth registration system, including the ability for Mexican citizens to obtain birth certificates at U.S. consulates. Only 3% of the population is now without ID.

Accelerating financial inclusion

Released in June 2016, the National Policy on Financial Inclusion sets out the road map for the Mexican government’s strategy. There are six key areas in the policy:

Financial education

One of the most important components of an effective financial inclusion plan is awareness and education. Mexico’s Ministry of Education will include financial education within the basic education curriculum, and financial training courses will be made widely available to the adult population.

Leverage technology

Although more than half of Mexico’s adult population lacks a bank account, a much higher proportion makes use of current technology. Nearly 90% of Mexicans possess a mobile phone, which opens the door to innovative solutions for financial inclusion such as mobile money and digital payments.

Develop financial infrastructure

Unfortunately, there are many gaps in terms of Mexico’s present financial infrastructure. The policy aims to promote partnerships between the government and the private sector to encourage the development of more financial services in underserved areas.

Improve financial services access and use

The Mexican government is committed to increasing both the levels of access to and use of formal financial services. Already, it has financially included close to 7 million women in poverty through the distribution of a government transfer debit card. Plus, more than 6 million households now have life insurance coverage, and previously excluded populations now benefit from business loans at preferential rates.

Protect financial services consumers

As with any system that handles money, consumers that use financial services should be adequately protected through effective regulation and enforcement. By making consumer protection a priority, the government wants to promote safer savings and public trust of financial institutions.

Financial inclusion measurement

There is also, of course, a need to be able to measure and quantify any progress made with Mexico’s financial inclusion initiative. To meet this need, the government plans to continue issuing its regular National Survey for Financial Inclusion and will provide support for academic research projects that will help to determine the policy’s success.

Considerations for growth

There are many positive trends happening in Mexico. It graduates over 120,000 engineers every year. eCommerce is growing at 6.5% annually and is expected to reach USD$21.8 billion by 2024. Mobility programs, especially in notoriously congested Mexico City, are taking off with many local players gaining traction. There is a high level of venture capital investment in Mexico, with $717 million being invested in 2019.

Improving financial inclusion and seeing increasing use of digital channels can have tremendous effects on the country. With more opportunities for financial services, eCommerce, digital education and other communication and transaction services, Mexico can quickly leapfrog many other economies around the world. Expanding into Mexico not only provides access to a large and growing market but also enables better access to all of Latin America. As the 20’s start to take shape, providing services to Mexico is an exciting and smart option for global growth.

With Trulioo GlobalGateway, you can instantly verify identities and businesses in Mexico. GlobalGateway provides coverage in over 100 countries, including surrounding LATAM countries, such as Chile, Costa Rica, Columbia, Ecuador, El Salvador and Venezuela. For specific coverage details, please contact Sales or book a demo to see global identity verification in action.

Solutions

Individual Verification

Simplify KYC Identity Verification Across the Globe

Resources Library

Know Your Customer

White Papers

Build Trust and Safety With Digital KYC

Featured Blog Posts

Business Verification (KYB)

Enhanced Due Diligence Procedures for High-Risk CustomersIdentity Verification

Proof of Address — Quickly and Accurately Verify AddressesBusiness Verification (KYB)

How to Verify Legitimate Businesses and Merchants